Connect with us

Connect with us

Jul 06, 2023

Jul 06, 2023

India’s future hangs in the balance as climate change looms large. Organisations need to follow a 2-pronged approach to combat this existential crisis.

The world has grown warmer by 1.1°C, and is well on its way to breaching the Paris Agreement target of 1.5°C and can reach beyond 2°C by the end of the century. As per the IMF, India is most vulnerable to climate-induced risks compared to other advanced economies and BRICS countries. These have far-reaching impacts on the Indian economy – up to 4.5% of India’s GDP is at risk by 2030 (source: McKinsey), 6% of the GDP could be lost by 2050 (source: World Bank), and this number will become 10% by 2100 (source: Overseas Development Institute). Organisations worldwide need to adapt and become resilient to the physical changes caused by climate change and transform themselves internally to mitigate climate change.

To effectively tackle climate change, organisations need to understand their exposure to key physical & transition risks and their financial implications.

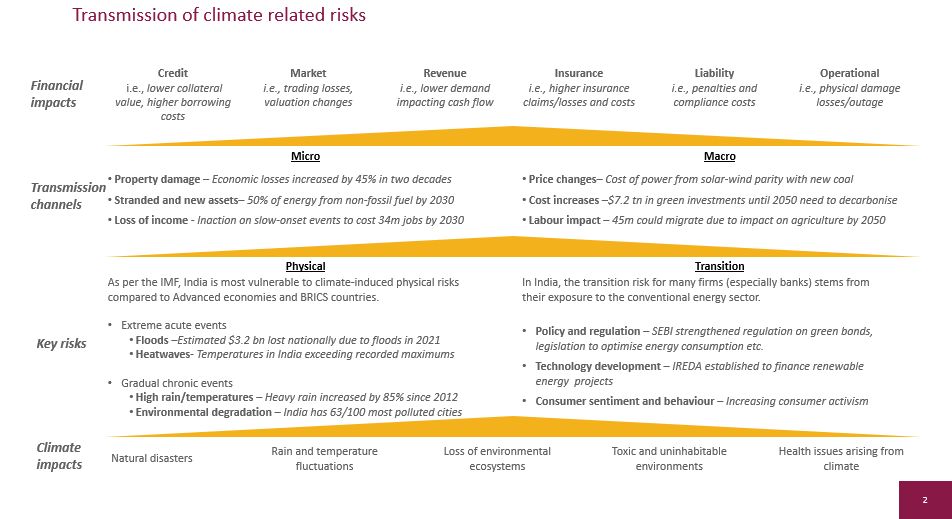

Figure 1: The transmission of climate-related risks with select examples from the Indian context.

Climate impacts refer to the direct consequences of climate change, such as rising global temperatures, increased frequency and intensity of extreme weather events (e.g., hurricanes, droughts, heat-waves), sea-level rise, and precipitation patterns.

Physical risks are the potential damage and disruptions from climate impacts. These can be further divided into extreme events and chronic events.

Transition risks arise from transitioning to a low-carbon and climate-resilient economy. These risks include policy and regulatory changes, technological advancements, market shifts, and consumer preferences.

Transmission channels refer to the pathways (micro and macro) through which climate impacts and transition risks can affect organisations.

Financial implications refer to the direct impact on an organisation’s financial resources, including credit (lower collateral/ higher risk ratings leading to higher interest rates), market valuation (valuation changes), revenue (decreased revenue leading to lower cash-flows), insurance (higher risk premiums), compliance (adhering to incoming regulations) and operations (physical damage/supply chain disruptions).

Organisations in India are ill-prepared to face these risks due to factors such as limited technical capacity, poor risk identification, and a lack of emphasis on green strategy.

Businesses lack the necessary resources, knowledge, skills, and expertise to understand and address climate-related risks adequately. A study of 154 credit and risk officers highlighted that only 17% are aware of specific standards or guidelines for assessing ESG lending risks (source: UKPACT). The absence of capacity often leads to a lack of risk identification within businesses. Climate risks are multidimensional and require a thorough assessment to identify potential vulnerabilities. 70% of the banks have not attempted to quantify the amount of their portfolio susceptible to climate risk (source: the RBI). Without a clear understanding of climate risks and their potential impact on the business, organisations struggle to formulate effective strategies that integrate sustainability into their operations and value chain. As per a survey, only a few companies are considering climate change under their Corporate Strategy (43%), Risk Management (43%) and Finance (32%) (Source: WTW).

These challenges can be efficiently addressed by implementing good climate governance driven by the board, executed by risk committees, and supported by incentives, culture, and data.

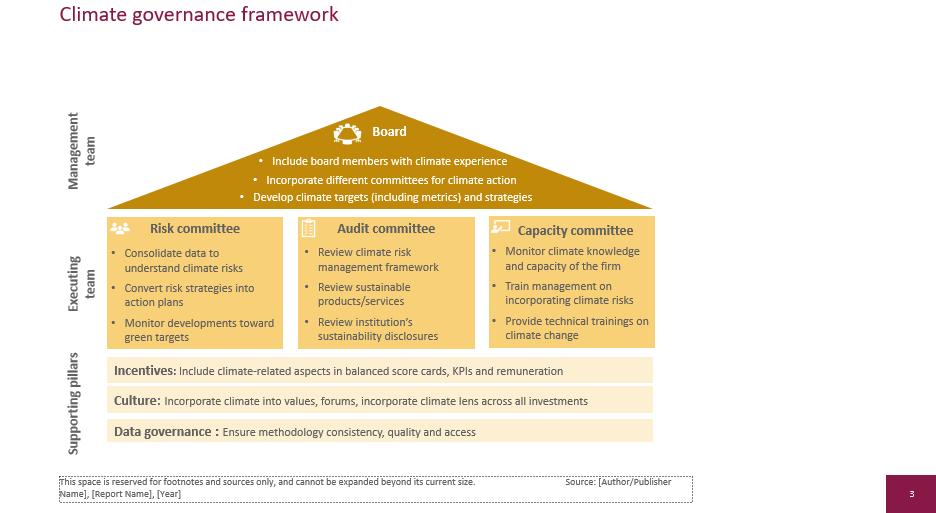

Figure 2: A climate governance framework

The Board can drive top-down climate agenda by embedding climate experience, establishing climate-focused committees, and setting climate targets & strategies.

To enhance climate governance, boards will benefit from hiring directors/experts with climate-related expertise and experience. E.g., Unilever’s Sustainability Advisory Council comprises independent external specialists in sustainability who guides their strategy. In India, many major companies, such as Mahindra & Mahindra, have a Chief Sustainability Officer responsible for identifying climate risks with the Chief Risk Officer.

Boards can establish dedicated risk committees or subcommittees responsible for assessing, monitoring, and reporting the organisation’s exposure to physical and transition risks and create green strategies. E.g., Barclays Bank has incorporated climate change into board audit and risk committees to establish targets and review progress.

Boards can actively participate in setting climate targets and developing strategies to achieve them. This involves establishing clear goals for reducing greenhouse gas emissions, increasing energy efficiency, transitioning to renewable energy sources, and other relevant sustainability metrics. E.g., In 2020, Apple committed to being 100 per cent carbon neutral for its supply chain and products by 2030. In India, Infosys became carbon neutral in 2020 and aims to reduce absolute Scope 1, Scope 2 GHG emissions by 75% and Scope 3 GHG emissions by 30%.

The Executing Committees created by the Board can help effectively carry out risk management, review risk disclosures and help build climate capacity within the organisation.

The Risk or Opportunity Committee can collate climate data from internal and external sources, including projections, exposure data, trends, policies, and best practices. It can assess risks, collaborate on mitigation & green strategies, and monitor progress towards green targets and climate commitments. E.g., Ford Motors has a sustainability committee which advises the company on the development of strategy, policies, and practices to address public sentiment and shaping policy in the areas of energy consumption, climate change, greenhouse gas and other criteria pollutant emissions, waste disposal, and water use.

The Audit Committee can oversee the organisation’s risk management framework, addressing climate-related risks. It can review and align green products/services with international standards. The risk audit committee can handle sustainability disclosures, including annual sustainability reports and climate reports. E.g., ITC’s sustainability governance structure is a board committee on sustainability supported by a sustainability compliance review committee.

The Capacity Committee can assess climate knowledge, provide targeted training for management on environmental risks and sustainability integration, and organise technical training for various departments to enhance climate capacity. E.g., Standard Chartered is working with Imperial College London, on a 4-year project to help build the capacity of the firm on climate risk management. In the Indian context, Tata Group designed a “Sustainability Leadership Programme” to help C-suite executives across the Tata Group understand the risks and opportunities posed by the rapidly changing climate.

The Board can further enhance climate governance by creating incentives, building a climate-driven culture, and ensuring data governance.

Incentives can be developed by linking remuneration (e.g., commissions/bonuses) with green initiatives and tracking the same through critical KPIs. E.g., 20+ large European banks have linked ESG with CEO’s variable pay (source: Capital Monitor). Organizations can integrate climate into their core values, create platforms for discussions and develop a climate lens (framework for actively incorporating climate across all its services/products). E.g., in 2012, Microsoft voluntarily introduced an internal carbon fee that holds its business units financially accountable for their carbon emissions. Wipro is actively involved in climate change advocacy through global forums like ‘Transform to Net Zero’ and World Economic Forum as well as through the CII Climate Change Council in India.

Finally, organisations can ensure that good quality climate data is collected by following international methodologies and developing MEL systems. E.g., UBS has a Data Management Office to ensure robust governance over climate data.

Moving forward, organisations can take inspiration from guidelines provided by national, regional, and international bodies.

In India, SEBI introduced the Business Responsibility and Sustainability Report (BRSR) in 2021, focusing on Environment, Social and Governance disclosures; on 20th February 2023, SEBI further released its ESG Committee’s recommendations on streamlining the ESG disclosures in India. The RBI, in its recent discussion paper on “Climate Risk and Sustainable Finance”, proposes good practices for climate governance on the lines of setting up board-level climate committees led by sustainability and risk experts to drive policy, strategy, risk management, monitoring, and disclosure.

The European central bank created a “good practices document” in 2022, which focuses on climate governance. Globally, Taskforce for Climate-Related Financial Disclosures (TCFD) has governance disclosures as one of its fundamental principles. The World Economic Forum developed a guidance note on “How to Set up Effective Climate Governance on Corporate Boards” in 2019.

In conclusion, climate governance is a complicated subject and can vary across geographies and sectors. There is an opportunity for organisations to create coalitions/collaborative platforms to further simply and contextualise it. International coalitions such as the “Climate Governance Initiative by World Economic Forum” are creating global collaborations in over 50 countries with over 100,000+ members. In India, although country-level partnerships such as the “Indian Climate Collaborative” exists, in order to truly realise the climate governance opportunity, sector-specific coalitions such as the “Indian Banking Association” must be set up to create, share and collaborate for the best governance practices.

QUOTE:

To effectively tackle climate change, organisations need to understand their exposure to key physical & transition risks and their financial implications.

He is a Sr. Consultant at Dalberg Advisors, focusing on climate change as a fellow, and has worked across various sectors ranging from climate change to agriculture, global health, and education. He has over 7+ years of experience in the consulting domain, from strategy to data & technology. He is an ex-entrepreneur and currently advises firms focusing on social impact. He is alum of the Indian School of Business, where he was a scholar of excellence.

He co-leads the climate practice at Dalberg Advisors and has over 20+ years of experience in climate change. Previously he was a Senior Policy Officer in Climate Change at the World Bank Group in Washington, DC, where he helped negotiate Climate Investment Funds (CIFs), a $10 billion fund, from a sunset clause to its recapitalisation. Till July 2022, he served as the Assistant Director-General of the International Solar Alliance (ISA). Previously, he has made significant contributions while working at the Green Climate Fund (GCF) and UNFCCC.

Owned by: Institute of Directors, India

Disclaimer: The opinions expressed in the articles/ stories are the personal opinions of the author. IOD/ Editor is not responsible for the accuracy, completeness, suitability, or validity of any information in those articles. The information, facts or opinions expressed in the articles/ speeches do not reflect the views of IOD/ Editor and IOD/ Editor does not assume any responsibility or liability for the same.

About Publisher

Bringing a Silent Revolution through the Boardroom

Institute of Directors (IOD) is an apex national association of Corporate Directors under the India's 'Societies Registration Act XXI of 1860'. Currently it is associated with over 30,000 senior executives from Govt, PSU and Private organizations of India and abroad.

View All BlogsMasterclass for Directors

Categories